New Financial Regulations to Cost Credit Card Companies $25B per Year

A rule proposed by the Federal Reserve in December of last year and scheduled to go into effect in April and the effects of other new regulations could cost credit card companies $25 billion in revenues per year, according to a report from Boston Consulting Group (BCG), a management consulting firm.

Debit Card Fees Going Down

The Durbin Amendment of the sweeping financial overhaul legislation (the Dodd-Frank legislation) passed last year, charged the Federal Reserve with ensuring that debit card interchange fees — the fees charged by card issuing banks each time one of their cards is used for payment — are “reasonable and proportional.” While no one doubted how the Fed will interpret the directive, the fee reduction it proposed in December was seen as a bit too drastic, even by some House Democrats, including Barney Frank, one of the co-sponsors of the Dodd-Frank legislation.

The Federal Reserve proposed that debit card interchange fees are limited at $0.12 per transaction, with several options on exactly how this could be done. According to the Fed’s own analysis, the new limit would be about 70 percent lower than the average fee of $0.44 per transaction last year.

“The amount the credit card companies are allowed to charge is too low,” Frank told CNBC’s Maria Bartiromo in an interview. “If they [the House Republicans] want to do something on it, I’ll work with them,” he added.

Bank Revenues Down by 29 Percent

Card issuers collected $16.2 billion from debit card interchange fees alone in 2009, according to the Federal Reserve. Based on the Fed’s analysis, if the proposed interchange fee limit on debit card transactions were in effect in 2009, the issuers’ revenues would have been only $4.86 billion, or $11.34 billion less.

Since then debit card use has increased, as debt-weary consumers slashed credit card spending and significantly reduced outstanding balances in the wake of the financial meltdown after the collapse of Lehman Brothers. There are now more than 500 million debit cards in circulation in the U.S.

The effects of the CARD Act of 2009 will also contribute to the issuers’ falling revenues. BCG’s report estimates that the combined effects of the changing financial regulatory landscape will cost banks about 29 percent, or $25 billion, of their total yearly retail transaction revenues.

Effect on Consumers

Unfortunately, while bank revenues from debit card fees is certain to go down, this is unlikely to translate into a win for consumers. Even if, unlikely as it may seem, retailers choose to pass the savings from lower interchange fees on to their customers, consumers will end up paying them back in other ways.

Banks are already looking for ways to recoup their expected losses. One option under consideration is charging checking account maintenance fees. According to one analyst, quoted by Reuters, a yearly fee of $30 – $40 per checking account would be sufficient to fully make up for the lost revenues. New technology and products will also help banks limit the damage, according to the BCG report.

So by most estimates the banks will be fine, once the dust settles. Retailers will also be better off, as they will be paying less for accepting debit card payments. What is not as clear is whether the regulations passed to protect consumers will end up causing us all to pay more for financial services than we used to. What do you think?

Image credit: Wikimedia Commons.

Why the U.S. Has not Adopted Chip-Based Credit Cards

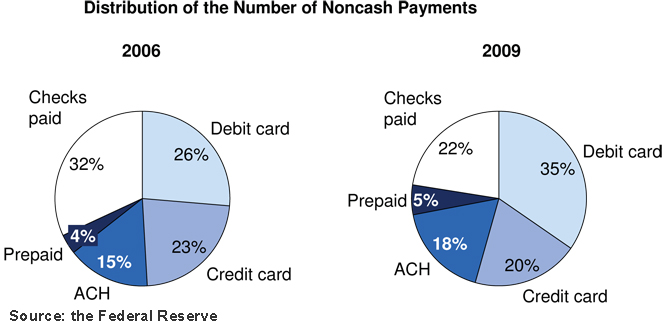

Americans Use More Prepaid, Debit Cards, Less Credit and Checks