Overview: Accepting Credit Card Payments Online

It is always amusing and often instructive to look at the credit card processing industry through the eyes of an outsider. Inc.com’s Christine Lagorio is the latest one to give it a shot in a recent article. She directs her attention to the online payment processing segment of the industry.

The author begins with an advice on how to select a payment processing service provider and mentions several names. She then goes on to review the part payment gateways play in the process and here is where it gets confusing. The article doesn’t explain what a gateway does, while it seems to be suggesting that it is all you need to accept payments online. This is a common misconception and we’ve had to separate the facts from the fiction in many conversations with our clients.

Payment gateway is a service that connects an e-commerce website’s shopping cart with the merchant’s processing bank and transmits transaction information between them. Once a customer places an order, the gateway encrypts the information, routes it to the processing bank and then relays the authorization response (approved, declined, etc.) back to the customer. It serves, for e-commerce stores, the same purpose that a physical point of sale (POS) terminal does for brick-and-mortar businesses.

The payment gateway, however, is just a component (although a vital one) of each e-commerce merchant account, just as the POS terminal is a part of a retail merchant account. Both services facilitate the capture and transmission of transaction information from the merchant to its payment processor. The secure transmission of transaction data is the principal use of a payment gateway. Once the information is sent to the processing bank, the transaction has to be authorized, cleared and settled, in order to be completed. This whole process, from the capturing of information, to the settlement and funding is what a merchant account service provides.

Lagorio also provides pricing information for several major gateways and correctly notes that payment processors use gateways as portals. What she has not mentioned is that processors also typically offer much lower gateway set-up and per-transaction costs than the gateway provider. For example, while Authorize.Net would set up an account for $99 and would charge $0.10 per transaction, a processor may set up an Authorize.Net account for $50 (or less) and charge less than $0.10 per transaction.

The biggest gap in Lagorio’s review, however, is perhaps the failure to explain what gateway authorization fees are and how they differ from the other per-transaction fees that merchants are charged. The $0.10 per transaction fee mentioned above is a gateway authorization fee. Authorization fees are charged solely for the use of a gateway or a POS terminal. For each bank card transaction, you will be charged an additional fixed fee, which is totally separate from the authorization fee. In her report Lagorio cites several examples, ranging from $0.21 – $0.25. It is important to add that you would be paying these fees, regardless of whether your provider is Authorize.Net, First Data or UniBul Merchant Services. These additional per-transaction fees are a component of the “discount fee” that processors charge for processing the merchant’s transactions. The other component of the discount fee is represented as a percentage of the transaction amount. So a typical e-commerce discount rate would be 2.19% + $0.25 per transaction. Discount fees are divided among three participants: the processing bank, the card issuing bank and the card association (Visa or MasterCard). The lion’s share of the discount fees, estimated at about 75% of the total processing fees U.S. merchants paid in 2008, is called interchange fee. It is published bi-annually by Visa and MasterCard and is collected by the card issuer. The association gets a fraction of one percent (about 0.1%), and the rest is collected by the processor.

Image credit: Justitsministeriet.dk.

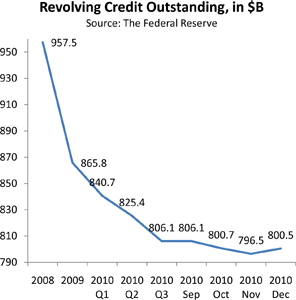

Consumer Credit Card Debt Up 3.5% after 27 Consecutive Months of Decline

12 Signs of E-Commerce Fraud