7 Steps to Preventing Card-Present Fraud

Preventing fraud is much more easily done in face-to-face credit card transactions, compared to payments accepted online or over the phone. After all, if in doubt you can examine the card for signs of altering or you can request that your customer provides a driver’s license to confirm his or her identity.

Yet, a face-to-face environment is only safer if you know how to take advantage of it. Here is a short list of seven simple steps you should take at the checkout when accepting Visa or MasterCard cards:

- Check the account numbers on the front of the card. Visa card numbers start with the number 4, MasterCard — with 5. The numbers are embossed (raised in relief) and should be clear and uniform in size and spacing. The last four digits of the account number on the front of the card should match the four digits printed on the signature panel on the back of the card. These numbers should not be chipped or otherwise altered in any way and you should not be seeing any “halos” of previous numbers under the embossed account number.

- Examine the hologram. Visa and MasterCard usually place their holograms on the front of their cards either above or below their brand marks. On some new cards, the hologram is located on the back or integrated into the magnetic stripe. Either way, the hologram is three-dimensional with interlocking globes (for MasterCard) or a flying dove (Visa) and should reflect light and appear to move when the card is rotated.

- Compare signatures. The card is invalid and you should not accept it, unless it is signed. You need to ensure that the signature on the cards matches the customer signature on the sales receipt. Make sure that the card’s signature has not been taped over, erased, or otherwise altered in any manner.

- Examine the magnetic stripe. The magnetic stripe should be smooth and straight, with no signs of tampering.

- Keep up-to-date with the new designs. Some new cards bear numbers that are unembossed. You will not be able to take a manual imprint of such cards, but they are not any less valid.

- Check the expiration date. Never accept a card past its “Good Thru” date. It may otherwise look completely legitimate, but the card is no longer valid and the transaction may be charged back.

- Verify that the customer is an authorized user. Only the cardholder can use the card. If in doubt — the signature does not match or the customer behaves in a strange manner — ask for a government-issued ID to verify your customer’s identity.

If you believe that a fraudulent transaction may be under way, you need to make a Code 10 call to your processing bank’s voice authorization center. You will be transferred to the card issuer and an operator there will ask you a series of “yes” and “no” questions to determine the validity of the transaction and will instruct you how to proceed.

Image credit: Mattsoldmanrants.com.

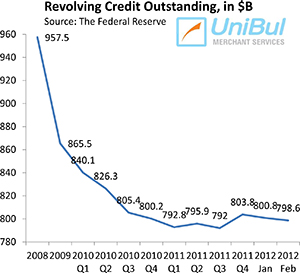

Credit Card Debt Keeps Falling and Americans Aren’t Done with It

Why Checkout Fees Are a Non-Issue