Managing Billing Descriptors

The way your company’s name appears on your customer’s credit card statement is called a billing descriptor. The billing descriptor is set up and managed by your payment processor. When you first fill out your merchant account application, you provide both your “Doing Business As” (DBA) name and your legal business name. Typically, your processor will use your DBA name as a billing descriptor. However, you should not take this for granted and should always check the way it is set up. Moreover, American Express’ payment system is set up to use your legal name as a billing descriptor, so you should take this into consideration as well.

Billing descriptors are particularly important for businesses accepting payments in a card-not-present environment, where there is no physical interaction between the merchant and the customer. In order for MO / TO and e-commerce merchants to qualify for the lower interchange rate offered to merchants operating in a card-not-present (Visa: CPS, MasterCard: Merit 1), the business’ name and customer service number must appear in the billing descriptor field.

Billing descriptor types:

- Default billing descriptor. If your company offers a single product or service, this descriptor would be sufficient. For example:

ABC SERVICES 800-111-2345.

This is the billing descriptor that your processing bank will set it up for you by default. - Soft billing descriptor. Some processors support a type of billing descriptor that allows the description field in the cardholder’s statement to be modified to include a more detailed description of the transaction. This is the soft billing descriptor type. The merchant’s name is usually truncated to three letters plus an asterisk, followed by a short description of the service or product that the business provides. Be advised that this field is usually limited to 25 characters plus the phone number. For example:

ABC* Instant Oil Change 800-111-2345.

If your business offers multiple lines of products or services, the soft billing descriptor may be a good asset to utilize. Be sure to check with your processor to see if they support this feature and for their format requirements.

It should be emphasized that for the majority of businesses, the default billing descriptor will be sufficient, regardless of the variety of merchandise. Convenience stores, for example, are well known to their customers by name, so there is no need to specify that the type of purchase is beverage, snack or something else. When your customer sees a charge on her statement from Pearl St. Convenience, she would immediately recognize it. If, however, you carry several lines of product, each with individual brand recognition, not related to your DBA name, you will probably need a soft billing descriptor. For example Symantec Corporation manufactures the Norton antivirus family of products, as well as other types of software. A customer who bought a Norton Internet Security package, however, may not know that, and if the billing descriptor shows Symantec, she may not recognize the charge.

Once you decide which type of billing descriptor is the best match for you, contact your merchant account provider and ask them to set it up that way. Some processors may have special requirements for the information that can be displayed, so you may have to be flexible. Yet, both your processor and you have an interest in setting up your billing descriptor in a way that makes it easy to identify a charge, because if your customer does not recognize your company’s name on his or her credit card statement, the transaction may be disputed and lead to a chargeback. Chargebacks are costly and everyone involved in processing them should try to keep them to a minimum.

Image credit: Webanywhere.co.uk.

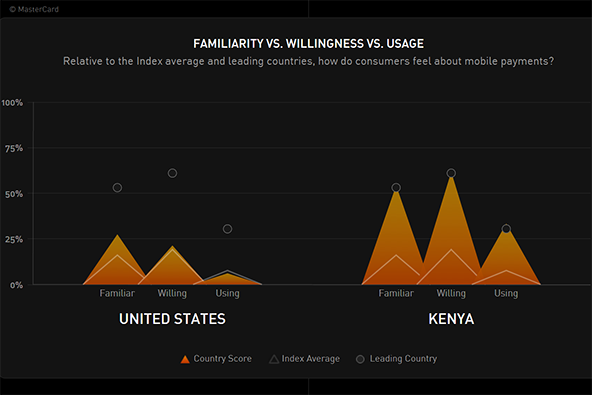

Shaping the M-Payments Future: Kenya vs. the U.S.

How Does an E-Commerce Merchant Account Work?

Do you know which credit card processors allow for soft descriptors or dynamic descriptors to be changed.