Paying down Credit Card Debt still Tops Americans’ Financial Priority List

The aggregate outstanding amount of consumer debt in the U.S. rose by less than anticipated in July — the 23rd consecutive monthly increase — we learn from the latest Federal Reserve consumer credit data release. The slower-than-expected growth was primarily the result of a drop in the credit card debt total, which fell for a second consecutive month, following a huge spike — the biggest one in years — in the month immediately before that that. As a result, the May increase in the card debt total is now more than fully reversed. And that should surprise no one — the latest data on credit card delinquency and default rates showed that, even as both of these measurements are either at or very near all-time record-lows, both of them kept falling in the last month. For as long as that trend continues, the credit card debt total will have nowhere to go but remain stagnant or even drop further.

The increase of the overall consumer debt total is the result of the uninterrupted growth of auto and student loans and is fueled by a continuing recovery in the housing market and an improving consumer confidence. Auto loans and student debt have been the main drivers of growth in consumer credit in the period following the financial crisis, whereas the credit card total has been virtually unchanged since around the end of 2010. However, the growth of the federal student loan total has slowed down considerably since the start of this year, which is actually good news, as delinquencies and defaults in this category have gone through the roof and keep rising. Let’s take a look at the latest Fed data.

Credit Card Debt down 2.6% in July

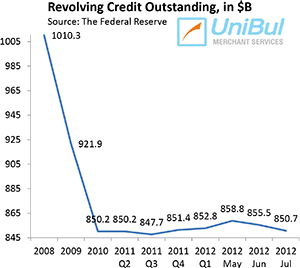

The aggregate consumer revolving credit in the U.S., which is made up almost exclusively of outstanding credit card balances, fell in July at a seasonally adjusted annual rate of 2.6 percent, or $1.8 billion, from the previous month’s level, after a bigger-than-initially-estimated 5.2 percent decline in June. The Fed’s revolving credit total began its free fall immediately following the collapse of Lehman Brothers in September 2008 — a process that continued until the end of 2010 when it stabilized at around its present level. Since then, it has remained mostly unchanged.

The aggregate consumer revolving credit in the U.S., which is made up almost exclusively of outstanding credit card balances, fell in July at a seasonally adjusted annual rate of 2.6 percent, or $1.8 billion, from the previous month’s level, after a bigger-than-initially-estimated 5.2 percent decline in June. The Fed’s revolving credit total began its free fall immediately following the collapse of Lehman Brothers in September 2008 — a process that continued until the end of 2010 when it stabilized at around its present level. Since then, it has remained mostly unchanged.

The total for July — $849.8 billion — is just 1.1 percent, or $9.1 billion, above the total reported at the end of 2010 ($840.7 billion) — at the height of the credit card debt deleveraging process. Moreover, the latest total is lower by 15.9 percent, or $160 .5 billion, than the all-time high of $1,010.3 billion measured at the end of 2008.

Overall Consumer Credit up 4.4%

The non-revolving portion of the U.S. consumer debt total, comprised of student loans, auto loans and loans for mobile homes, boats and trailers, but excluding home mortgages and loans for other real estate-backed assets, continued to increase, in keeping with a long-standing trend. The Federal Reserve reported a $12.2 billion — or 7.4 percent — increase in July from June’s level, bringing the total up to $2,002.3 billion — the first time ever the non-revolving debt has exceeded the $2 trillion threshold. That followed a downwardly revised 9.5 percent increase in June.

The non-revolving portion of the U.S. consumer debt total, comprised of student loans, auto loans and loans for mobile homes, boats and trailers, but excluding home mortgages and loans for other real estate-backed assets, continued to increase, in keeping with a long-standing trend. The Federal Reserve reported a $12.2 billion — or 7.4 percent — increase in July from June’s level, bringing the total up to $2,002.3 billion — the first time ever the non-revolving debt has exceeded the $2 trillion threshold. That followed a downwardly revised 9.5 percent increase in June.

As you can see in the chart to the right, the non-revolving debt component of the total didn’t plummet nearly as precipitously as the revolving one in the aftermath of the financial crisis and then it was much quicker to resume its rise.

Demand for federal student loans continued to be strong in July, though it has been much weaker in recent months compared to last year. The Fed report tells us that lending to consumers by the federal government — primarily educational loans — increased by $2.5 billion for the month to $571.9, following a downwardly revised $3.3 billion increase in June. As you can see in the chart to your right, growth in this segment has slowed down considerably since January of this year when we saw the last truly big increase — $25.9 billion. Overall, since the end of 2008, when it was only $104.3 billion, the total of outstanding federal government loans to American consumers has increased by a stunning 448.3 percent, or $467.6 billion.

Demand for federal student loans continued to be strong in July, though it has been much weaker in recent months compared to last year. The Fed report tells us that lending to consumers by the federal government — primarily educational loans — increased by $2.5 billion for the month to $571.9, following a downwardly revised $3.3 billion increase in June. As you can see in the chart to your right, growth in this segment has slowed down considerably since January of this year when we saw the last truly big increase — $25.9 billion. Overall, since the end of 2008, when it was only $104.3 billion, the total of outstanding federal government loans to American consumers has increased by a stunning 448.3 percent, or $467.6 billion.

Helped by still-low interest rates, though slightly higher than in previous months, cars and trucks kept selling very well in August, at a 16 million annualized rate — the fastest since November 2007, according to Businessweek, and up from 15.6 million in July.

In all, with the sole exception of August 2011 when it fell by 5.2 percent, the non-revolving component of the debt total has increased in every month since July 2010. The figure for July was higher by 23.8 percent, or $384.9 billion, than the pre-crisis peak of $1,617.4 billion, reported five years earlier in July of 2008.

In all, with the sole exception of August 2011 when it fell by 5.2 percent, the non-revolving component of the debt total has increased in every month since July 2010. The figure for July was higher by 23.8 percent, or $384.9 billion, than the pre-crisis peak of $1,617.4 billion, reported five years earlier in July of 2008.

The aggregate amount of outstanding U.S. consumer credit — the sum of its revolving and non-revolving portions — rose by 4.4 percent, or $10.4 billion, to $2,852.1 billion in July. That new total is greater by $264.7 billion, or 10.2 percent, than the pre-Lehman record-high of $2,587.4 billion, reported, once again, in July 2008.

The Takeaway

So there isn’t any new trend that the latest Fed consumer debt data have revealed. Even as Americans keep taking out ever more auto loans and continue to pile up student debt, they remain stubbornly reluctant to borrow more on their credit cards. And, considering the latest data on credit card delinquencies and charge-offs, it looks as though we should expect more of the same in the coming months. Each one of the six biggest U.S. card issuers reported lower charge-off rates in July and all but two (Citigroup and Capital One) also reported lower delinquencies.

Overall, the late payments rate in the U.S. fell for the fifth month in a row, reaching a new record-low of 1.3 percent in July and the charge-offs fell by another quarter of a percent to 3.37 percent, according to Fitch Ratings. Even more impressively, Fitch’s monthly payment rate (MPR) — measuring the portion of their total credit card debt paid by Americans at the end of each month — rose by almost 2 percent in July to a new all-time high of 26.05 percent and there is every reason to expect it to remain high. And for as long as the MPR is at current levels or close, credit card debt will not be an issue.

Americans Continue Slashing Credit Card Debt

Business Owners Don’t Understand Credit Card Processing