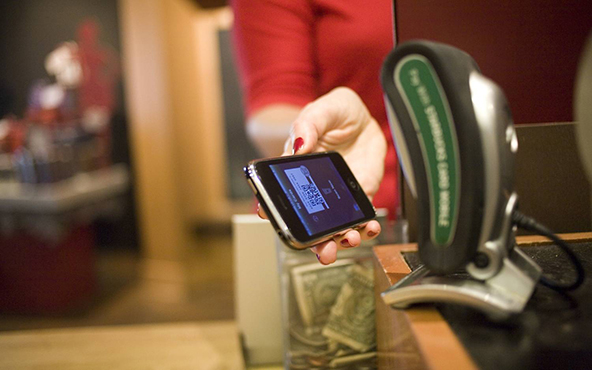

How to Handle PIN-based Debit Transactions

We had been completely neglecting PIN-based debit on this blog until a close review of the Federal Reserve’s debit interchange rule told us that this particular type of transactions will actually become marginally more expensive to process under the new?ápricing structure, which was supposed to achieve exactly the opposite result.

Since then we’ve begun to make amends and have posted a couple of articles on PIN-based debit. In this post I will expand on the subject by reviewing the basic PIN-based transaction rules that must be complied with at the point of sale.

Transaction Processing

All point-of-sale (POS) terminals that process PIN-based debit must be encrypted before being used. The encryption process is handled by the processor or an authorized service provider. The credit card companies (e.g. American Express and Discover) and Associations (i.e. Visa and MasterCard) have developed mandatory encryption standards, so make sure your processor is compliant.

Each PIN debit transaction begins by swiping the card through a POS device and then the cardholder authenticates him- or herself by entering their PIN (except in some special circumstances). The following requirements apply:

- Authorizations. Only transactions that have received an authorization approval should be completed.

- Pre-authorizations. Pre-authorization requests must be initiated using a cardholder PIN and for a specified amount. Funds cannot be transferred until a pre-authorization completion response is received for the transaction amount. Completing a pre-authorized transaction does not require the use of PIN or a POS terminal.

- Partial pre-authorizations. Merchants initiating pre-authorization requests must support the processing of partial pre-authorizations.

- Cardholder identification. The cardholder PIN is normally used for identification, unless both:

- Technical problems prevent the cardholder from entering the PIN and

- The merchant chooses to use a sales draft to be signed by the cardholder who is also asked to provide identification.

- PIN privacy. The merchant is not allowed to ask the cardholder to reveal his or her PIN.

- Balance inquiries. A balance inquiry can only be completed at a POS terminal with a PIN.

- Credit transactions. A credit transaction can only be initiated if the cardholder provides the sales receipt from the original transaction and must:

- Be processed to the same card and within one year of the original transaction date.

- Be initiated through the use of a PIN and at a POS terminal.

- Be for an amount equal to or less than the original transaction amount.

- Be initiated from the same merchant (not necessarily at the same merchant location).

Processing Transaction Reversals

A transaction can be reversed electronically if the reversal is done on the same settlement day as the original transaction. The following requirements apply:

- A reversal must be initiated at the same merchant location where the original transaction was processed.

- The card must be read by a POS terminal.

- The cardholder must re-enter his or her PIN.

- The merchant must transmit the trace number and the exact amount of the reversal.

Transaction Receipt

The merchant is required to provide the cardholder with a transaction receipt that includes all of the following information:

- Transaction amount.

- Transaction date.

- Transaction type (e.g., sale, credit, reversal).

- Only the last four digits of the account number.

- Merchant name and location.

- Trace number.

The Takeaway

The fact that the new interchange pricing structure is much more favorable for merchants processing signature-based rather than PIN-based debit transactions does not mean that you should switch to the latter arrangement. Remember that what matters for you is the overall discount your processor charges you. Interchange is only a part of this discount and will remain the same, regardless of whether your customers authenticate themselves through a PIN or a signature.

On a separate note, now that Visa has made it mandatory for all U.S. processors to support acceptance of chip-based transactions by April 1, 2013, it seems likely that in the not-too-distant future all card transactions may become PIN-based. Yes, chip-and-PIN cards are different from their mag-stripe counterparts, but, from a cardholder’s point of view, the use of either type is indistinguishable from the other.

Image credit: Merchantjuice.com.

Why Starbucks’ Platform Is Not the Best Way Forward for Mobile Payments

How to Verify E-Commerce Transaction Information

Dear Sir/Madam,

I would like you to publish articles related to Merchant frauds like,

1) Fly by night frauds

2) Direct Debit frauds(Merchant setlling the account without proper authorization codes)

Reagrds,

Niraj Singh

Fraud Prevention Manager- Card Product

Only a smiling visitor here to share the love (:, btw outstanding style and design. “Everything should be made as simple as possible, but not one bit simpler.” by Albert Einstein.

Thank you, johnshue! Simplicity was definitely one of the objectives we were pursuing with the new design.

I have not checked in here for a while as I thought it was getting boring, but the last few posts are good quality so I guess I will add you back to my everyday bloglist. You deserve it my friend :)

Hi Hilary,

We are trying to make every post worth reading, but not all topics are interesting to everyone.

I’m not sure exactly why but this site is loading incredibly slow for me. Is anyone else having this issue or is it a problem on my end? I’ll check back later and see if the problem still exists.

Great post and right to the point. I don’t know if this is actually the best place to ask but do you people have any idea where to get some professional writers? Thank you :)

I keep listening to the news broadcast talk about getting free online grant applications so I have been looking around for the best site to get one. Could you advise me please, where could i get some?