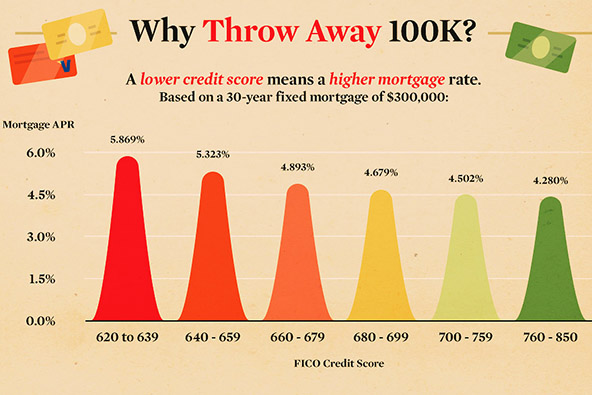

E-Commerce Dynamic Currency Conversion

Processing international credit card transactions, settling in foreign currencies and currency conversion on e-commerce websites are topics that I am often discussing with merchants. Their requirements vary and different types of set-ups are usually needed, but often enough the solution is fairly straightforward and simple to implement. It is called Dynamic Currency Conversion (DCC).

What is Dynamic Currency Conversion?

DCC is a credit card processing service that enables U.S. businesses to offer their international customers the option to pay in their own currency, in addition to U.S. dollars. DCC is currently available for Visa and MasterCard transactions only, both in face-to-face and card-not-present environments.

Now, U.S. businesses can accept foreign-issued bank cards perfectly well without DCC, however, the currency used in such transactions is always the one in which the merchant settles. Moreover, merchants are charged additional fees for accepting foreign-issued cards, which can be quite steep (typically in the range 0.50% – 1% of the transaction amount).

How Does DCC Work?

The DCC service supports 36 foreign currencies at present and the transaction process at participating merchants goes through the following stages (in an e-commerce setting):

The DCC service supports 36 foreign currencies at present and the transaction process at participating merchants goes through the following stages (in an e-commerce setting):

- The customer enters his or her payment information at the checkout.

- The DCC-enabled software determines if the card has been issued by a foreign bank.

- The exchange rate for the customer’s home currency is calculated by adding the wholesale interbank rate and the merchant’s foreign currency fee.

- The converted amount is displayed to the customer and they are asked to select between paying in U.S. dollars or their own currency.

- If the foreign currency is chosen, the transaction receipt will show the exchange rate including conversion fees, the U.S. dollar amount and the foreign transaction amount (see sample receipt at right).

It turns out, perhaps unsurprisingly, that most customers choose to pay in their own currency, even though the aggregate currency conversion fee charged on DCC transactions is often higher than the one charged by the card issuer.

I don’t think it would be much of a stretch to suggest that at least some customers would not have completed a transaction, if the option of paying in their local currency was unavailable.

DCC: Merchant vs. Consumer Perspective

So, if a merchant’s volume is sufficiently high to offset the DCC maintenance fees, I see no reason not to use the service, provided the processor supports it. The merchant would still be paying the foreign transaction fee charged by the processor, but would be able to make up for it by charging its customers a conversion fee.

From a consumer’s perspective, things look quite differently. Using DCC at the checkout is typically a very expensive way to complete a transaction. The DCC currency conversion fee is almost certain to be substantially higher than the issuer’s foreign transaction fee (3% is the prevalent rate in the U.S., however Capital One charges no such fee).

Image credit: Burbuja.info.

Banks Stand to Lose $12B from Debit Card Fee Reduction

On Rising Inequality, Household Borrowing and the Financial Crisis